July 09, 2024

Madison Capital Group Launches Car Wash Venture

Madison Capital Group is proud to announce their latest venture, Links Car Wash, an innovative car wash on a mission…

Read More

August 26, 2025

Links Car Wash is well-positioned to leverage federal tax incentives to optimize its express car wash operations. Bonus depreciation can be particularly advantageous for a capital-intensive business like express car washes, where investments in equipment and facilities are substantial. This article explains how bonus depreciation strengthens our investment model at Links Car Wash, LLC. We’ll cover the foundational changes introduced by the Tax Cuts and Jobs Act of 2017 (TCJA), the subsequent phase-out schedule, and the recent reinstatement of full bonus depreciation under the One Big Beautiful Bill Act of 2025 (OBBBA). Note that while this is based on current federal tax rules as of August 2025, tax laws can change, and professional consultation is recommended for your specific filings.

What Is Bonus Depreciation?

Links investors benefit from immediate tax deductions through bonus depreciation—allowing most of their investment to be written off in Year 1, reducing taxable income and enhancing cash flow.1

Unlike standard depreciation, which spreads the cost recovery over the asset’s useful life (e.g., 5 years for equipment or 39 years for buildings), bonus depreciation accelerates tax savings by providing an upfront deduction. This reduces taxable income immediately, improving cash flow for our investors. Qualifying property generally includes:

Property must be new or used (as expanded under TCJA), acquired by purchase (not inheritance or gift), and placed in service during the tax year. Exclusions include land, inventory, and property used outside the U.S. more than 50% of the time.

For Links Car Wash, this incentive is especially valuable because our operations involve heavy investment in specialized equipment and improvements. Examples of qualifying assets for our business might include:

Cost segregation studies can further optimize this for Links Car Wash by reclassifying portions of our facilities (e.g., 65%–100% of a car wash’s value) into shorter-life categories eligible for bonus depreciation, rather than lumping everything under the 39-year building category. In some cases, the IRS views nearly the entire car wash structure as eligible due to its specialized use.

The Tax Cuts and Jobs Act of 2017: Expanding Bonus Depreciation

The TCJA, enacted in December 2017, significantly enhanced bonus depreciation to stimulate business investment. Prior to TCJA, bonus depreciation was temporary and varied (e.g., 50% under earlier extensions), but it often lapsed or required congressional renewal.

Key changes under TCJA:

For Links Car Wash, this meant you could deduct the full cost of new tunnels, automated systems, or site improvements in Year 1, rather than over 5–15 years. This was a game-changer for our industry, enabling faster expansion and mergers/acquisitions. For instance, if Links Car Wash invested $1 million in qualifying equipment, you could claim a $1 million deduction, potentially saving $210,000–$370,000 in federal taxes (depending on your tax bracket).

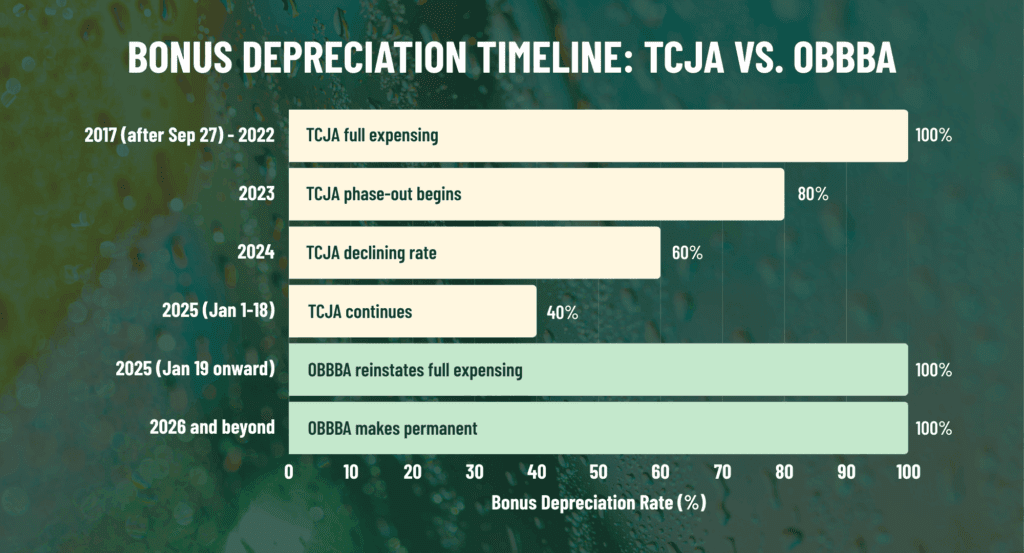

The Phase-Out Schedule Under TCJA

To make the tax cuts revenue-neutral over time, TCJA included a phase-out of 100% bonus depreciation starting in 2023:

This schedule applied unless extended by future legislation. For 2025, without intervention, Links Car Wash would have been limited to a 40% first-year deduction, with the remainder depreciated under MACRS rules. For our operations, this phase-out could have slowed investment, as partial deductions reduce the incentive for large capital outlays like new sites or upgrades.

The One Big Beautiful Bill Act of 2025: Reinstatement and Enhancements

Enacted in July 2025, the OBBBA (H.R. 1, 119th Congress) represents a major tax reform package aimed at extending and expanding TCJA provisions. Often referred to colloquially as the “big beautiful bill,” it addresses expiring TCJA elements and introduces new incentives.

Regarding bonus depreciation, OBBBA reinstates 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. This effectively overrides the 40% phase-out for 2025, providing full expensing similar to the TCJA’s peak years. The reinstatement is retroactive only to January 19, 2025, so assets placed in service earlier in the year may still fall under the 40% rule unless they qualify under transition provisions.

For Links Car Wash, this restoration should reignite investment by allowing full write-offs for new builds or acquisitions, potentially boosting our M&A activity and greenfield development.

Application to Links Car Wash: Practical Considerations

Links Car Wash and its investors stand to gain substantially from bonus depreciation due to our asset mix. A typical setup for one of our locations might include:

To maximize benefits for Links Car Wash:

Recapture rules apply if an asset is sold before full depreciation, treating the bonus as ordinary income.

Investor Benefits: Leveraging Bonus Depreciation for Enhanced Returns

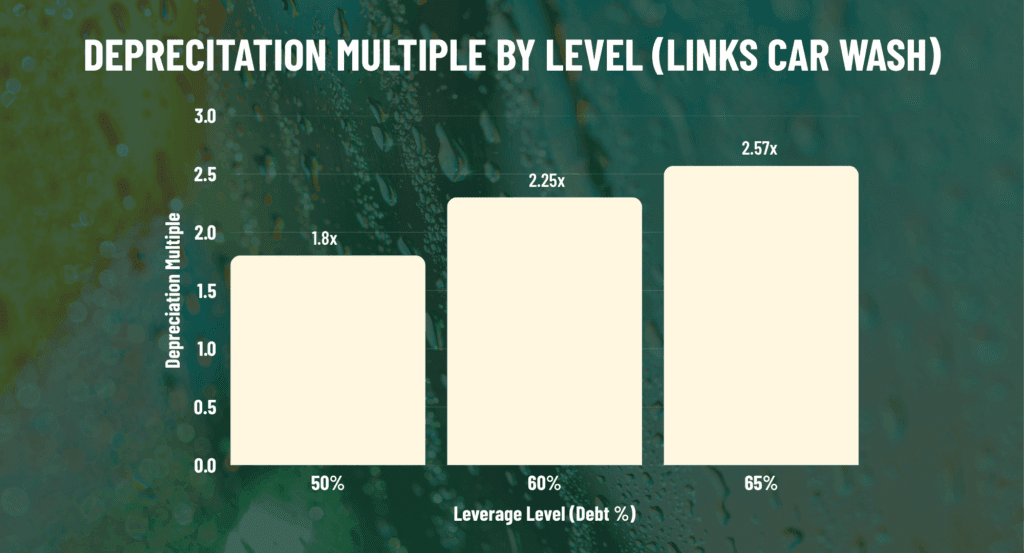

At Links Car Wash, bonus depreciation is strategically utilized to enhance returns for investors by accelerating tax deductions, which can significantly reduce taxable income and improve after-tax cash flows. A key metric we target is a 1.8 depreciation multiple, meaning we aim to generate $1.80 in first-year deductions for every $1.00 of investor equity. For example, if an investor contributes $100,000, our goal is to structure the investment such that they receive $180,000 in bonus depreciation deductions in Year 1. This is achieved through the high eligibility of car wash assets for 100% bonus depreciation, often covering nearly the entire purchase price minus non-depreciable land value.

Using leverage—financing purchases with debt—further amplifies this depreciation multiple. When acquiring a car wash, the bonus depreciation deduction applies to the full cost basis of the qualifying assets, regardless of how much is financed with debt. This means investors can deduct the entire eligible amount while only committing a portion of the total cost as equity. For instance, if a $1 million car wash (with $900,000 in depreciable assets) is purchased with 50% debt ($500,000 loan) and 50% equity ($500,000), the $900,000 deduction on $500,000 equity yields a 1.8x multiple. Higher leverage ratios (e.g., 60-70% debt, common in stable cash-flow businesses like car washes) can push this multiple even higher, as the equity denominator decreases while the deduction remains tied to the full asset cost. This strategy not only boosts investor returns through deferred taxes but also supports portfolio growth by freeing up capital for additional investments.

Conclusion

Bonus depreciation, supercharged by TCJA and revived by OBBBA, offers Links Car Wash a powerful tool for tax efficiency and growth. By allowing immediate deductions on key assets, it frees up capital in the competitive express car wash business. By maximizing bonus depreciation, Links delivers stronger after-tax returns and fuels rapid portfolio growth—creating long-term value for our investor community.

Disclaimer: This article is for informational purposes only and is not intended as tax advice. Readers should not rely on this information for making tax-related decisions and should consult their own tax professionals for advice tailored to their specific circumstances.

Authored by: Joe F. Teague, Jr., Esq., CEO of Links Car Wash

Madison Capital Group is proud to announce their latest venture, Links Car Wash, an innovative car wash on a mission…

Read More

Links Car Wash is thrilled to announce the single-site acquisition of Floris Car Wash on McCoy Rd in Orlando, Florida.

Read More

Links Car Wash is excited to announce its first location in Charlotte, NC at 5301 North Tryon Steet.

Read More

Links Car Wash is excited to announce its continued expansion in the Sunshine State with two new Fort Myers locations.

Read More

Links Car Wash is excited to announce the acquisition of a development site off E. Colonial Drive, marking the company’s…

Read More

Links Car Wash is thrilled to announce the acquisition of Blue Penguin Car Wash, located off Ulmerton Road in Largo,…

Read More

Links Car Wash is excited to announce the acquisition of four new locations in Florida, including three Jallo Car Wash…

Read More

Links Car Wash is proud to announce its continued expansion in Florida with the acquisition of two new locations, further…

Read More

Links Car Wash is excited to announce the opening of its first Tampa location at 3451 E. Busch Blvd.

Read More

Links Car Wash is proud to announce the acquisition of a new development site located at 1800 West Blue Heron…

Read More

Links Car Wash celebrated the completion of its rebrand and facility upgrades with a ribbon-cutting event earlier today at 3893…

Read More

Links Car Wash, a rapidly emerging leader in the express car wash sector, is closing out 2024 with exceptional success…

Read More

Links Car Wash proudly hosted a ribbon-cutting ceremony at its newly remodeled location at 3451 E. Busch Boulevard.

Read More

Links Car Wash’s grand opening weekend event raised $3,680 benefiting Big Brothers Big Sisters of Tampa Bay and Big Brothers…

Read More

Links Car Wash proudly celebrated the opening of its newest location at 5311 N Tryon Street. This marks a significant…

Read More

Links Car Wash is growing its Florida footprint with the acquisition and redevelopment of Sunset Car Wash on Sunset Point…

Read More

Links Car Wash is expanding in Orlando with a new property at 4089 S Goldenrod Rd, Orlando, FL 32822. This…

Read More

Links Car Wash is proudly announces the official opening of its first North Carolina location at 5311 N. Tryon Street…

Read More

Links Car Wash is growing again in Florida with the opening of its newest location in Leesburg, FL. This expansion…

Read More

Links Car Wash proudly celebrated the grand opening of its newest location at 1000 South 14th Street in Leesburg, FL,…

Read More

Originally published by Auto Laundry News on March, 1st, 2025. Written by Timothy Denman. The old adage, “a chain is…

Read More

Links Car Wash recently celebrated the grand reopening of its newest location in Largo, Florida, at 6701 Ulmerton Rd.

Read More

Links Car Wash is proud to announce the grand opening of its first South Carolina location at 1109 E Liberty…

Read More

Links Car Wash officially marked its entrance into South Carolina with a celebratory ribbon cutting at its newest location, 1109…

Read More

Links Car Wash continues its expansion in Florida with the opening of a second Tampa location at 14504 Basswood Avenue. …

Read More

Links Car Wash officially celebrated the opening of its newest Tampa location with a ribbon-cutting ceremony at 14504 Basswood Avenue.

Read More

Links Car Wash is proud to announce the grand opening of its first Texas location at 5500 Altamesa Boulevard in…

Read More

Links Car Wash continues to expand its Florida footprint with the grand opening of its newest location at 6800 4th…

Read More

Links Car Wash proudly celebrated the grand opening of its first Texas location with a ribbon-cutting ceremony at 5500 Altamesa…

Read More

Links Car Wash is proud to announce the acquisition of two additional express car wash locations, strengthening its presence in…

Read More

Links Car Wash is excited to announce the launch of its new Fleet Program, designed to make it easier for…

Read More

Links Car Wash is proud to announce the opening of its first official location in the Fort Myers area, located…

Read More

Links Car Wash proudly celebrated the grand opening of its newest location at 9200 Daniels Parkway on Thursday afternoon.

Read More

Links Car Wash is proud to celebrate one year of delivering an elevated car wash experience with a one-day-only Anniversary…

Read More

Links Car Wash is proud to announce the success of its One-Year Anniversary $1 Ultimate Wash Day, which supported First…

Read More

Last week was a big one for Links Car Wash as the company completed the acquisition of twelve new express…

Read More

Links Car Wash wrapped up 2025 on a strong note with the acquisition of three additional properties across Florida and South Carolina.

Read More

Links Car Wash, a fast-growing express car wash company and affiliate of Madison Capital Group, is proud to announce the…

Read More

Links Car Wash and Fresh Stop, fast-growing brands under Madison Capital Group, today announced the addition of two senior leaders…

Read More

Links Car Wash is thrilled to announce that its newest location is now open at 215 Monitor Drive in Anderson. This is…

Read More